Among the many provisions in the multi-trillion-dollar legislative package being debated in Congress is a provision that would eliminate a strategy that allows high-income investors to pursue tax-free retirement income: the so-called back-door Roth IRA. The next few months may present the last chance to take advantage of this opportunity.

Roth IRA Background

Since its introduction in 1997, the Roth IRA has become an attractive investment vehicle due to the potential to build a sizable, tax-free nest egg. Although contributions to a Roth IRA are not tax deductible, any earnings in the account grow tax-free as long as future distributions are qualified. A qualified distribution is one made after the Roth account has been held for five years and after the account holder reaches age 59½, becomes disabled, dies, or uses the funds for the purchase of a first home ($10,000 lifetime limit).

Unlike other retirement savings accounts, original owners of Roth IRAs are not subject to required minimum distributions at age 72 — another potentially tax-beneficial perk that makes Roth IRAs appealing in estate planning strategies. (Beneficiaries are subject to distribution rules.)

However, as initially passed, the 1997 legislation rendered it impossible for high-income taxpayers to enjoy Roth IRAs. Individuals and married taxpayers whose income exceeded certain thresholds could neither contribute to a Roth IRA nor convert traditional IRA assets to a Roth IRA.

A Loophole Emerges

Nearly 10 years after the Roth's introduction, the Tax Increase Prevention and Reconciliation Act of 2005 ushered in a change that relaxed the conversion rules beginning in 2010; that is, as of that year, the income limits for a Roth conversion were eliminated, which meant that anyone could convert traditional IRA assets to a Roth IRA. (Of course, a conversion results in a tax obligation on deductible contributions and earnings that have previously accrued in the traditional IRA.)

One perhaps unintended consequence of this change was the emergence of a new strategy that has been utilized ever since: High-income individuals could make full, annual, nondeductible contributions to a traditional IRA and convert those contribution dollars to a Roth. If the account holders had no other IRAs (see note below) and the conversion was executed quickly enough so that no earnings were able to accrue, the transaction could potentially be a tax-free way for otherwise ineligible taxpayers to fund a Roth IRA. This move became known as the back-door Roth IRA.

(Note: When calculating a tax obligation on a Roth conversion, investors have to aggregate all of their IRAs, including SEP and SIMPLE IRAs, before determining the amount. For example, say an investor has $100,000 in several different traditional IRAs, 80% of which is attributed to deductible contributions and earnings. If that investor chose to convert any traditional IRA assets — even recent after-tax contributions — to a Roth IRA, 80% of the converted funds would be taxable. This is known as the "pro-rata rule.")

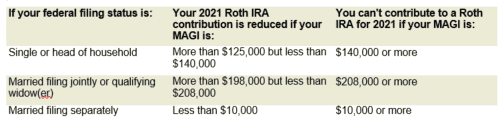

Current Roth IRA Income Limits

For 2021, you can generally contribute up to $6,000 to an IRA (traditional, Roth, or a combination of both); $7,000 if you'll be age 50 or older by December 31. However, your ability to make contributions to a Roth IRA is limited or eliminated if your modified adjusted gross income, or MAGI, falls within or exceeds the parameters shown below.

Note that your contributions generally can't exceed your earned income for the year (special rules apply to spousal Roth IRAs).

Note that your contributions generally can't exceed your earned income for the year (special rules apply to spousal Roth IRAs).

Now or Never ... Maybe

While no one knows for sure what may come of the legislative debates, the current proposal would prohibit the conversion of nondeductible contributions from a traditional IRA after December 31, 2021. If you expect your MAGI to exceed this year's thresholds and you'd like to fund a Roth IRA for 2021, the next few months may be your last chance to use the back-door strategy. Contact your financial and tax professionals for more information.

Have specific questions? Don't hesitate to reach out to me today

Wes Garner, CRPC

Principal Wealth Strategist

(281) 269-8669

wgarner@tdecu.org

There is no assurance that working with a financial professional will improve investment results.

You can make 2021 IRA contributions up until April 15, 2022, but if the legislation is enacted, a Roth conversion involving nondeductible contributions would have to be conducted by December 31, 2021.

Keep in mind that a separate five-year rule applies to the principal amount of each Roth IRA conversion you make, unless an exception applies.

Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly.

The information provided is not intended to be a substitute for specific individualized tax planning or legal advice. We suggest that you consult with a qualified tax or legal professional.

LPL Financial Representatives offer access to Trust Services through The Private Trust Company N.A., an affiliate of LPL Financial.

This article was prepared by Broadridge.

LPL Tracking #1-05203927